When it comes to tax education-especially tax education for small business owners- it almost seems like there is a stigma around asking questions or admitting that you don’t know everything. We would REALLY like to REMOVE that stigma. Nobody is born understanding tax laws (though that would have been really helpful on the CPA exam).

We ALL have to start somewhere when learning how taxes work. And while taxes may be easier to understand and, dare I say, fun for some people to do while they are harder for others to understand. We believe that every business owner who wants to understand their financials and taxes can and should be allowed to ask all the questions that they want to ask.

And yes, you can absolutely go read the tax code and get all the info first hand… You absolutely should if you want to. However, it can be a bit confusing for the average non accountant, so the purpose of this article is to make it EASIER for you, as a non accountant, to understand taxes.

Understand Taxable Income

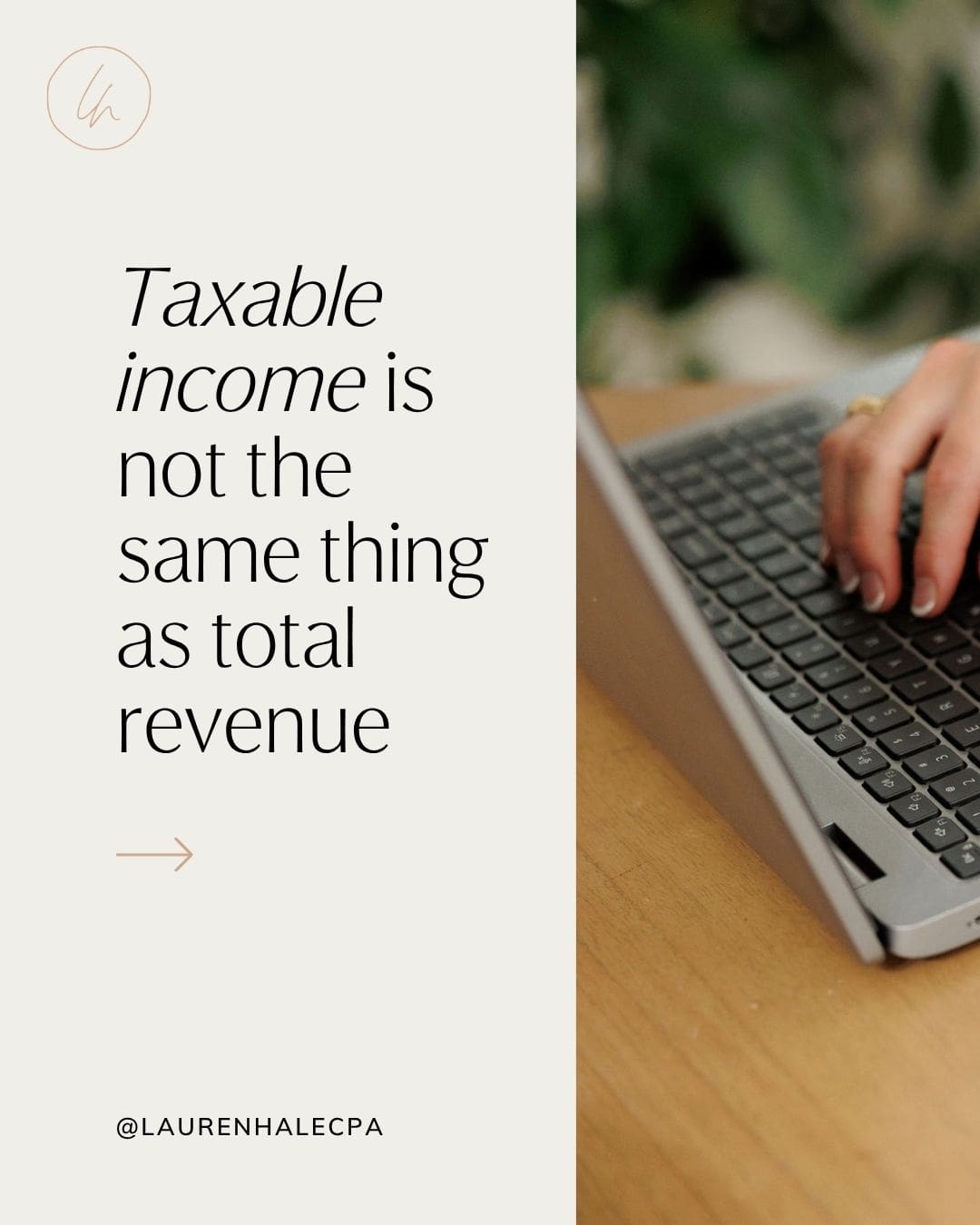

If you only walk away from this article understanding one thing, let it be this: taxable income is not the same thing as total revenue.

Your business may have strong gross income for the year, but does not necessarily mean that the entire amount is subject to income tax.

Taxable income is calculated after allowable deductions are applied under current tax laws. Ordinary and necessary business expenses reduce what is actually taxed.

For example, if your business brings in revenue from services, product sales, or real estate activity, that total becomes part of your gross income. From there, legitimate expenses such as payroll, rent, supplies, insurance, contractor payments, and professional services are deducted.

(P.S. That social media joke trend of calling a brand new vehicle a “desk” for tax purposes- fake news.)

The amount that remains is generally what determines your income tax and self employment tax.

Pro tip: This is all the more reason why accurate bookkeeping is absolutely vital. If income and expenses are not recorded correctly, your income tax return will not reflect what actually happened.

Tax Brackets and What That Actually Means and What It Doesn’t Mean

Tax brackets are very often misunderstood. (So if you don’t understand tax brackets, no shame).

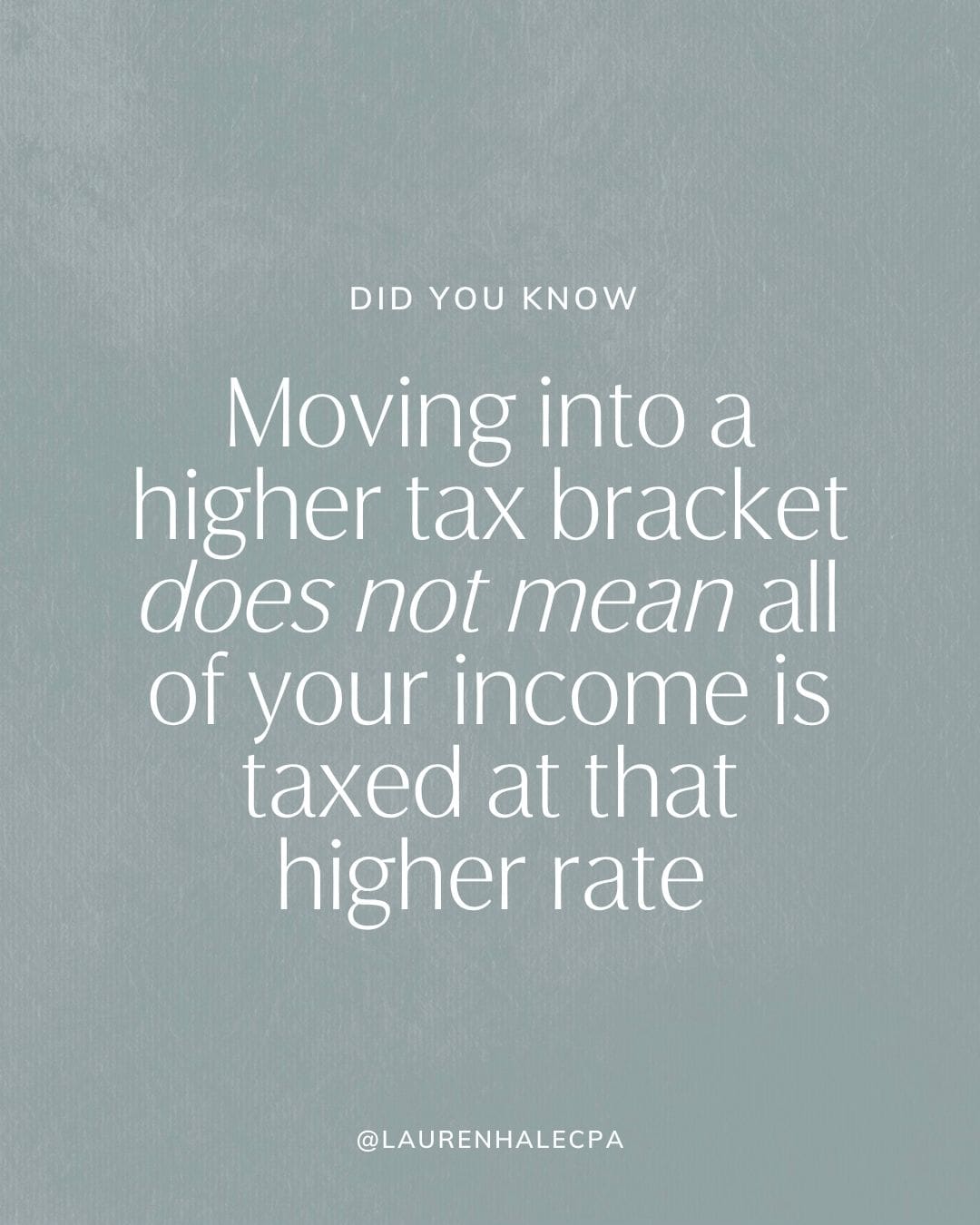

More than one small business owner out there has looked at the tax brackets for the year, and thought “oh no, I’m going to move up a whole tax bracket!” their on the bubble income, But slow down, take a deep breath. Moving into a higher tax bracket does not mean all of your income is taxed at that higher rate. The United States uses a progressive system. Different portions of your taxable income are taxed at different percentages.

Only the income that falls within a specific bracket is taxed at that bracket’s rate.

So if your income increases, only the portion that crosses into the next bracket is taxed differently. The rest remains taxed at the lower rates.

Understanding how tax brackets function removes a lot of unnecessary fear around earning more money.

Tax Deductions

Tax deductions reduce taxable income. They do not reduce your tax bill dollar for dollar.

Common deductions for business owners include expenses that are ordinary and necessary for your business type. (I.E why a brand new lambergini does not qualify as a “desk” for your office) This may include rent, utilities, payroll, supplies, insurance, equipment, marketing, or software.

Believe it or not, not every expense qualifies. Certain conditions must be met under existing tax laws and financial regulations. Expenses must be legitimate and directly related to operating your business.

Remember: A deduction lowers the income that is taxed.

Tax Credits

Tax credits reduce your tax liability directly- ie dollar for dollar.

If you qualify for a $1,000 tax credit, your tax bill is reduced by $1,000.

When it comes to types of tax credits, there are business credits and personal credits. Some education credit opportunities include the American Opportunity Tax Credit and the Lifetime Learning Credit.

These apply when qualified higher education expenses are paid to an eligible educational institution and the student meets eligible student requirements. Income thresholds and documentation requirements apply.

There are also provisions related to qualified student loan interest and certain tax free distribution rules tied to education savings plans.

Credits operate differently than deductions, and the distinction matters when calculating what you actually owe.

Pro tip: Check with your accountant to see which credits may apply to you each year.

Filing Taxes

Filing taxes means submitting the required tax forms that report income, deductions, and credits.

Your filing obligations depend largely on your business type.

A sole proprietor files differently than a partnership. An S corporation files differently than a C corporation. If you file a joint return, both spouses’ income is reported together.

Your income tax return is the official record of your financial activity for the year. If an error is discovered later, an amended return may be necessary.

Paying Taxed

Paying taxes is often where business owners feel the biggest shift.

Employees are used to taxes being withheld automatically. Business owners are usually responsible for making estimated payments throughout the year.

Estimated taxes are generally paid quarterly and cover both income tax and self employment tax.

If sufficient payments are not made under the required conditions, penalties can even apply- adding to that tax bill you owe to Uncle Sam.

Planning for estimated taxes helps prevent large balances due at year end and supports steadier cash flow management.

Can I File My Taxes Myself?

In some cases, yes!

If your situation is straightforward, you don’t have multiple schedule C’s, not a lot of out of the ordinary deductions, then yes, self filing may be appropriate. Lots of people use software such as TurboTax or H & R Block. However, as the complexity of your tax return increases, the margin for error increases.

If you operate multiple entities, manage real estate, have significant tax liabilities, or file a joint return with multiple income sources, working with a CPA might save you more money than it costs you.

Truly, being able to file your own taxes is not about pride. It is about whether your situation calls for professional tax education and oversight.

The Difference Between Bookkeeping, Accounting, and Tax Preparation

So maybe you think. “Well I have someone doing my books.” and mistakenly think that you don’t need to have someone help prepare your taxes. However, there is a difference!

Bookkeeping records categorizes your transactions (what you spend money on, and what category it falls into). Bookkeeping tracks income and expenses.

Accounting interprets those numbers. It analyzes profitability, margins, and cash flow.

Tax education explains how tax laws apply to those numbers.

Bookkeeping determines gross income. Accounting evaluates performance. Your tax preparer fits all of your income and expenses into the current year tax laws to help you pay the taxes that you owe, but not any more.

Pro Tip: This is one of the reasons why we love being able to offer BOTH tax preparation and bookkeeping services in house. It helps everyone to be on the same page. Reduces confusion, and ultimately helps you have a more cohesive and holistic financial picture.

How Your Business Type Impacts Your Taxes

Your business type does more than determine how you registered with the state. It directly affects how your income is reported, how you are taxed, and how money moves from your business to your personal income tax return.

Let’s break that down in normal human words.

Sole Proprietorships

If you operate as a sole proprietorship, there is no legal separation between you and your business for tax purposes. The profit from your business flows directly onto your personal income tax return. That means you are typically responsible for both income tax and self employment tax on the net profit.

Partnership

A partnership works similarly in that the business itself generally does not pay income tax. Instead, profits are allocated to each partner, and each partner reports their portion of the income on their own return. Even if profits are left inside the business bank account, they may still be taxable to the partners depending on the structure.

Corporations

An S corporation operates differently. The business files its own tax return, but the profit generally passes through to the owners. Many S corporation owners pay themselves a salary, which is subject to payroll taxes, and then may also receive distributions. The way compensation is structured matters because it affects self employment tax and overall tax liabilities.

A C corporation is taxed at the corporate level first. If profits are distributed to owners as dividends, those amounts may be taxed again at the individual level. That is what people refer to when they talk about “double taxation.”

Real Life Application

Now, let’s talk about how that applies to real life.

- If you file a joint return, your spouse’s income may push you into different tax brackets.

- You own rental real estate in addition to your primary business, that income may be treated differently depending on whether it is considered active or passive.

- Your entity structure is changed mid-stream without understanding the tax implications, you may create reporting issues you did not anticipate.

Your business type influences how gross income is calculated, how tax liabilities are assessed, and how much flexibility you have in planning ahead. It is not simply a legal checkbox. It is a tax decision that affects everything downstream.

Estimated Taxes and Why They Surprise So Many Business Owners

One of the more common adjustments for new business owners is getting used to paying taxes without automatic withholding.

When you are an employee, income taxes and payroll taxes are withheld from each paycheck. You rarely have to think about setting that money aside because it is handled for you.

When you move into business ownership, that changes. Your revenue comes in without taxes withheld, and you are responsible for setting aside and submitting estimated payments throughout the year.

Estimated taxes are typically paid quarterly and are intended to cover both income tax and self employment tax as you earn income. Instead of paying one large amount at the end of the year, the system spreads the obligation across four payments.

The difficulty is that business income is not always consistent. Some months are stronger than others. Expenses fluctuate. It can be challenging to accurately estimate taxable income without regular review of your financials.

If estimated payments are not made in sufficient amounts under certain conditions, penalties may apply. In many cases, the issue is not intentional neglect. It is simply a lack of clear understanding at the outset.

Quarterly review and planning make this process far more manageable. When you know what to expect and build it into your cash flow decisions, estimated taxes become part of the rhythm of running a business rather than a surprise at year end.

What Actually Triggers an Audit and What Doesn’t

Audits tend to instill more fear than they actually deserve, mostly because people are not sure what actually causes them or what walking through an audit actually looks like.

In reality, many audits begin with something fairly simple: a mismatch. If the income you report does not align with the information the IRS receives from third parties, such as 1099s or W-2s, that discrepancy can prompt a closer look. Significant deductions that appear unusually high compared to gross income in your industry may also raise questions. Repeated losses in certain types of businesses can sometimes draw attention as well.

That said, not every amendment or deduction is a red flag.

Filing an amended return does not automatically trigger an audit. Discovering an error and correcting it is part of responsible reporting. Claiming legitimate deductions that meet the requirements of tax laws is also not something to avoid out of fear.

Claiming legitimate deductions does not automatically trigger an audit either. If an expense meets the requirements under current tax laws and you have documentation to support it, you should not leave it off your return out of fear.

What matters most is whether your numbers are accurate and supported. Consistent reporting and organized records go a long way in reducing unnecessary issues.

The Difference Between Tax Preparation and Tax Strategy

Tax strategy and tax preparation are two often confused terms. To put it simply, tax preparation looks backwards at what already happened while tax strategy looks ahead. Tax preparation is the process of taking everything that already happened during the year and reporting it accurately on your income tax return in compliance with current tax laws. It is necessary, it is important, and it ensures that your numbers are complete and correct.

Tax strategy happens earlier. It happens while decisions are still being made.

Instead of asking, “How do we report this?” strategy asks, “What happens if we do this?” It considers how purchasing equipment, adjusting compensation, changing your business type, or shifting income from one year to the next might affect your overall tax liabilities before those decisions are finalized.

You can learn tax rules through online tax courses or self study courses, and that knowledge absolutely has value. But strategy is what happens when those rules are applied thoughtfully to your specific situation, your cash flow, and your long term goals.

Preparation looks back at the year. Strategy shapes what the year becomes. A good place to start; with these three things small business owners should consider when starting the tax planning process.

Understanding Education Credits

Education related credits can play a role in your overall tax picture, especially if you or your children are paying for college or continuing education.

Two of the most common credits are the American Opportunity Tax Credit and the Lifetime Learning Credit. Both are tied to qualified higher education expenses paid to an eligible educational institution, but the rules for each are slightly different. Eligibility depends on factors like income levels, enrollment status, and whether the student meets the specific requirements outlined in current tax laws.

In addition to those credits, there may be deductions related to qualified student loan interest, and certain education savings accounts come with their own tax free distribution rules. The details matter, and documentation is important if you plan to claim any of these benefits.

Even though these credits are not directly tied to operating your business, they can still affect your overall tax liabilities, particularly if you file a joint return and household income is being considered together.

Common Tax Myths Small Business Owners Believe

There are a few misunderstandings that come up over and over again in conversations with business owners.

One of the most common is the belief that if the business does not show a profit, there are no taxes to worry about. In reality, other income sources may still create tax liability, and self employment tax can apply even when margins are tighter than expected. The full picture matters more than one line on a profit and loss statement.

Another misconception is that any business expense eliminates the same amount of taxes owed. Deductions do reduce taxable income, which is helpful, but they do not erase tax liability dollar for dollar. The actual savings depend on your overall income and tax bracket.

There is also confusion around LLCs. Forming an LLC is an important legal step, but it does not automatically change how you are taxed. An LLC is a legal designation. The tax treatment depends on how the entity is classified for federal tax purposes. Those are two separate decisions, even though they are often discussed together.

The Real Goal of Tax Education

The goal of tax education is not to memorize tax laws or to be able to win a debate with your local CPAs. It is not to complete an introductory course or pursue professional tax education (unless that is your career path).

The goal is to understand your tax liabilities and how taxes work in general well enough to make informed decisions without fear!

And ultimately, it is about stewarding your resources wisely and leaving a family legacy that you can be proud of.

Ready to have someone on your team who knows tax law inside and out AND cares about explaining things to you? Book a free consult here.